Allegro & InPost mutual dependency analysis

In today's edition, I analyze the relationship between Allegro, Poland's largest e-commerce platform, and InPost, the dominant automated parcel locker operator.

At the outset, I'd like to welcome new subscribers. And thank you all for your trust and for being here. I write for myself, BUT knowing how many people have been reading this is my greatest reward. Thank you for being here!

I write about topics that genuinely fascinate me. Here, you'll find thoughtful analyses at the intersection of business and technology. I uncover underlying mechanisms and describe what truly drives our modern world, looking beyond surface-level trends. If you seek intellectual stimulation, broader context, and engaging content, you've come to the right place.

I'll admit that this rivalry caught me somewhat by surprise. When placing an order on Allegro, the Paczkomat (parcel locker) didn't appear at the top of the list as the first choice option.

Packages from Amazon and Louge by Zalando were delivered by InPost. For the first time, I ordered something from Vinted - a package was ordered to a parcel locker. Changes and visibility limitations appeared. Information emerged that packages "from Allegro" can be collected at Żabka stores.

The relationship between Allegro, Poland's largest e-commerce platform, and InPost, the dominant automated parcel locker operator, represents one of the most interesting cases of interdependence in the Polish business ecosystem. This strategic relationship has lasted since 2014, evolving over time and changing the balance of power, risks, and dependencies. The partnership began in 2014 when InPost won the tender to deliver packages for Allegro. In the early years, both companies were more dependent on each other. Allegro accounted for nearly 62% of InPost's volume and 47% of its revenue. This synergy and interdependence shaped the Polish e-commerce market for the following decade.

In 2020, InPost and Allegro signed a framework agreement that was updated in January 2024. This agreement, crucial for both entities, defines pricing levels, minimum volumes, and adjustment mechanisms. The deal encompasses two main operating mechanisms:

Direct payments for deliveries within the Allegro Smart program

Courier selection by sellers independently of Allegro

Then, as if in complete clarity, the thought struck me: who has more to lose if rivelery unfolds, who grew on whom, and who might benefit from this? Today's post is my attempt to organize this into one coherent whole and understand what we can expect.

"This makes you my competitor... You're not my son. You're just a little piece of competition."

Daniel Plainview, There Will Be Blood

So I thought I'd be nice to delve into the numbers and think it through.

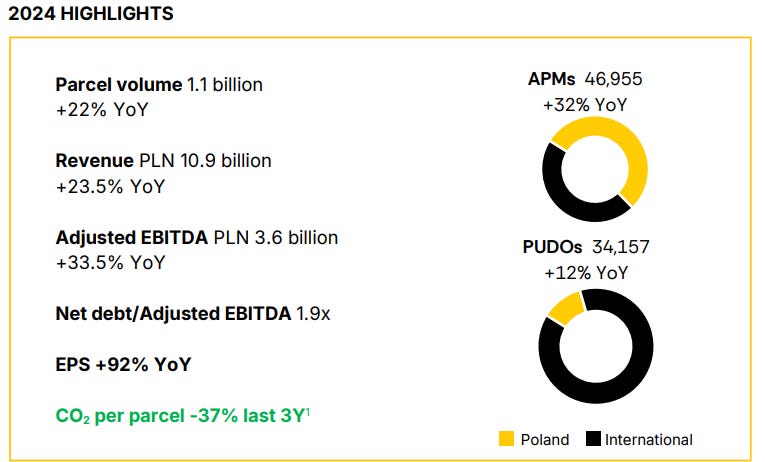

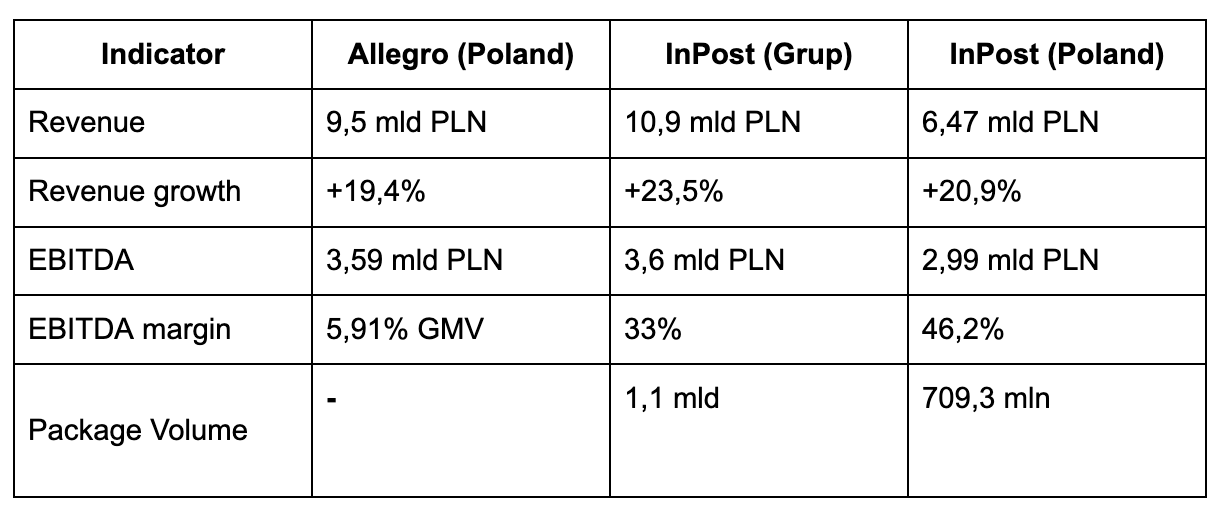

In 2024, InPost delivered a record 1.1 billion packages across the entire group, including 709.3 million in Poland (20% YoY growth). Currently, InPost operates over 26,500 parcel lockers in Poland, which represents approximately 70% of all available automated machines in Poland. The coverage density of InPost APMs within a 7-minute walking distance hit 64% nationwide, and nearly 90% in urban areas. In 2024, InPost made significant advancements in operations in Poland, adding seven new automated sorters and 11 new logistics sites. Across all of Europe, this amounts to over 50,000 machines. InPost's largest foreign markets are the United Kingdom and France (approximately 10,000 machines each at the beginning of 2025).

Allegro & InPost key numbers:

InPost is a Polish logistics technology company founded in 2006 by Rafał Brzoska that has revolutionized last-mile delivery across Europe through its network of over 47,000 automated parcel machines (APMs) spanning nine countries. Launched initially during a Polish postal strike as a workaround to state monopolies, InPost has evolved into Europe's dominant out-of-home delivery platform. The Company's core innovation lies in providing 24/7 accessible, self-service parcel collection and sending through strategically located metal lockers in shopping centers, gas stations, and residential areas, which customers access via a mobile app used by 13 million active users.

Revenue: 6,47 bilion PLN (+20.9% YoY) —> mainly due to higher volumes YoY

Adjusted EBITDA: 2,99 bilion PLN (+21.0% YoY)

EBITDA Margin: 46.2% (flat compared to the previous year)

Market Share: approximately 45% of the entire qualified market

Free Cash Flow: 1,59 bilion PLN for 2024 (up 32.5% YoY) —> highly cash-generative business model

Allegro is Poland's dominant e-commerce marketplace, founded in 1999 by Dutch entrepreneur Arjan Bakker as an eBay-inspired auction site that has evolved into Central Europe's most successful online shopping platform, commanding 45-50% of Poland's entire e-commerce market. Operating as a third-party marketplace connecting over 163,000 active merchants with 20.8 million buyers across six countries (Poland, Czech Republic, Slovakia, Hungary, Slovenia, and Croatia).

GMV: 60.71 billion PLN (+10.8% YoY)

Revenue: 9.5 billion PLN (+19.4% YoY)

Adjusted EBITDA: 3.59 billion PLN (+21.3% YoY)

Active Buyers: 15.1 million (+7.8% YoY)

Allegro Smart Subscribers: 7 million (double-digit YoY growth)

Allegro Pay: 10.8 billion PLN worth of loans originated

The Allegro platform accounts for approximately 1% of Poland's GDP, making it a key entity in the Polish economy.

EBITDA Performance Comparison:

InPost: 33.3% EBITDA margin (FY 2024),

Allegro: 5.91% EBITDA margin of GMV (FY 2024),

InPost's Poland segment maintains 46.0% margins, highlighting domestic market strength

CAPEX Plans for 2025: Allegro targeting PLN 0.85-1.0bn (+60-90% increase), focused on logistics infrastructure; InPost allocating 63% of CAPEX internationally.

Financial Leverage Metrics:

Allegro Net Leverage: 0.77x (Q4 2024) well within 1.0x ± 0.5x target range.

InPost Net Leverage: 1.9x (Q3 2024) improved from 2.6x year-over-year

Return Metrics: InPost ROIC of 13.50% demonstrates efficient capital deployment.

Analysis of mutual dependency

Customer diversification

Currently, Allegro represents a significantly smaller percentage of InPost's business. According to current data, Allegro accounts for approximately 30% of InPost's revenue in Poland and about 18% of the entire group's revenue. This is a significant change compared to 2020, when Allegro accounted for 62% of package volume. I believe this risk and consistent mitigation have been visible for some time. InPost has methodically and effectively diversified its partner/client base. Currently, InPost's largest client is Lithuanian Vinted, which accounts for 23% of the group's sales. Allegro Smart represents approximately 31% of InPost's revenue in Poland. InPost also handles deliveries for Zalando & Lounge by Zalando, Amazon Poland, Media Expert, IKEA, CCC, OLX, and x-kom.

Despite numerous efforts and initiatives, Allegro remains significantly dependent on InPost. It's estimated that InPost handles over 60% of all Allegro transactions. This is particularly visible in the context of Allegro Smart program subscribers, where InPost delivers more than 50% of all orders. This buyer's preference for delivery method is clear.

Logistical challenges and costs:

Allegro's delivery costs surged 22.9% to PLN 2.84 billion in 2024, representing up to 25% of total revenue.

Allegro plans to add 2,500 more postal automated machines in Poland in 2025.

Currently, Allegro owns over 5,000 automated machines (July 2025).

24% of package volume was managed by Allegro in Q4 2024.

The entire Allegro network (automated machines and pickup points) within Allegro Delivery comprises over 29,000 points.

"We cannot enter into alliances until we are acquainted with the designs of our neighbors." Sun Tzu, The Art of War

Strategic initiatives: Allegro

On one hand, we had diversification at the partner and client level. On the other hand, Allegro undertook several actions aimed at reducing dependence on InPost and their logistics network, which has become the standard for end customers. The key to minimizing dependence and mitigating this risk is expanding the Allegro Delivery network and investing in infrastructure.

Allegro Delivery:

4,500 Allegro One Box automated machines.

6,200 ORLEN Paczka automated machines.

6,500 DHL BOX 24/7 automated machines.

Over 45,000 pickup points in total after adding Żabka stores.

Infrastructure Investments:

Adding 2,500 new automated machines in 2025.

Partnerships with DHL eCommerce Poland and ORLEN Paczka.

Development of Allegro One Kurier service.

What certainly speaks in favor of Allegro is its 40% share of the Polish e-commerce market. Many people predicted Allegro's end when eBay entered the Polish market, as well as when Amazon announced it. Allegro is doing well and has maintained its position. Allegro possesses a powerful base of approximately 15.1 million active buyers in Poland. Certainly, beyond the diversification described above in the logistics area, it's worth noting the fact and possibility of directing traffic to selected/preferred logistics operators (which can also bring better prices and quality for the end customer). There's also a kind of strength in the ability to build and develop a network of 29,000 pickup points within Allegro Delivery.

The Battle for logistical independence

Currently, InPost's largest client is Lithuanian Vinted, which accounts for 23% of the group's sales. In 2024, Vinted achieved revenue of 813.4 million EUR (+36% YoY), Net Profit: 76.7 million EUR (+330% YoY), EBITDA: 158.9 million EUR (+100% YoY). I must admit I smiled slightly at these figures. I need to take a closer look at Vinted.

Other strategic areas:

International expansion, especially in the UK, France, and other European countries.

Improving brand visibility in the EU.

Investments in automation and operational efficiency.

InPost has advantages in several areas, including:

Dominant market position: Handling >70% of all parcel points in Poland

Parcel locker availability and network density: 64% of the population has access to a machine within a 7-minute walk.

Consumer trust, market position, and consumer preference: 68% of Polish consumers prefer pickup from automated parcel lockers.

Customer satisfaction with quality: NPS at 77.

Cost Efficiency Metrics: InPost parcel lockers cost €2.18 (9.15 PLN) - 35% lower than traditional courier services (€3.39/14.24 PLN).

Comparison of Key Financial Indicators 2024

UOKiK investigation signals high probability of regulatory intervention

The Polish competition authority launched formal proceedings in May 2024 following documented consumer complaints about automatic switching from InPost parcel lockers to Allegro Delivery during checkout. This represents a 70-80% probability of enforcement action based on:

Investigation Scope and Evidence:

Consumers document a systematic pattern of delivery method changes.

Video evidence shows automatic switching without user consent.

UOKiK's established enforcement history (€206 million Allegro fine in 2022).

Additional greenwashing charges were filed in July 2025, with potential penalties of up to 10% of turnover.

Market Impact Quantified:

InPost shares have declined over 20% since early 2024.

Specific 5-6% stock drop following Allegro's FY2024 results announcement.

Investor concerns about volume losses post-2027, when the partnership expires.

Management Strategic Responses:

InPost CEO Rafał Brzoska publicly criticized Allegro's "obvious conflict of interest".

Allegro CFO Jon Eastick confirmed developing "cheaper alternatives" while acknowledging higher InPost costs in 2025.

Both companies are positioning for potential regulatory constraints on self-preferencing

Price pressure

Pricing relations between companies evolve according to indexation agreements. In 2024, InPost introduced price increases for Allegro services of 4.9%, while previously the companies had agreed on a system of flexible increases based on the volume of delivered packages.

Who needs whom more?

This analysis and post are driven solely by my curiosity and do not constitute investment advice. Based on everything I managed to gather, I would risk the statement that Allegro needs InPost more than InPost needs Allegro, but this asymmetry is systematically decreasing.

"All happy companies are different: each one earns a monopoly by solving a unique problem. All failed companies are the same: they failed to escape competition."Peter Thiel, Zero to One

Arguments for greater Allegro dependency:

60% of Allegro transactions still go through InPost.

Customers prefer InPost automated machines due to network density.

Building a competitive network requires massive investments

InPost offers the highest quality and reliability of deliveries. Looking at the numbers, as a user, a better experience wins.

Arguments for greater InPost dependency:

Allegro still represents approximately 30% of InPost's revenue in Poland

Allegro is a large partner in the Polish e-commerce market that generates huge volumes that are difficult to replace

Complete loss of Allegro as a client could negatively impact InPost's results, stock price, position, and plans

Additional considerations

As the Allegro <> InPost relationship develops, new players may appear in the market:

InPost: 25,700 parcel lockers (48% market share)

DPD: 9,900 automated machines (18% market share)

Orlen: 6,200 automated machines (12% market share)

Allegro BOX: 4,500 automated machines (11% market share)

Żabka: 9 200 pick up points.

Competition may accelerate the development of new solutions. Greater competition may impact pricing for end customers. The influence of AI, along with changing shopping experiences and customer preferences, should also be considered. As Rafał Brzoska, CEO of InPost, predicts: "The future belongs to minimalist and hyper-personalized solutions." Thanks to AI, applications and platforms will identify customer needs and independently present product recommendations. The whole process is supposed to lead to the disappearance of classic marketplaces.

Consumer behavior insights

Parcel Locker Preference Dominance: 81% of Polish online shoppers prefer parcel lockers as primary delivery method this validates InPost's strategy but also highlights dependency risk for both companies.

Basket Value Evolution: Average basket increased from PLN 233 (€54) in 2020 to PLN 304 (€70) in 2023, showing 30% growth in consumer spending per transaction.

Return Behavior Specifics: Only 17% of consumers have never returned a product, with one-third using parcel machines for returns. I sense that the experience of returning parcels with InPost is a strength. But this has significant implications for reverse logistics costs and InPost revenue streams.

Same-Day Delivery Demand: 83% of consumers would shop more if same-day delivery was available, suggesting both opportunity and competitive pressure for faster service.

Demographic Spending Patterns: 38% of millennials (26-41 years) buy online multiple times per week.

As an investor, what I'll especially have a keen eye for is:

InPost's ability to maintain margins while reducing dependence on Allegro.

InPost revenue growth (10.9 billion PLN (€2.60 billion) with 23.5% YoY growth). How will this be scaled?

Diversification and expansion of InPost's client portfolio.

Effectiveness of Allegro's diversification strategy in reducing logistics costs.

CAPEX on Allegro's side.

The development pace of alternative delivery networks in Poland.

The impact of AI and the use of new technologies on shaping the entire market.

Network Utilization Standards: Target utilization rate of 70-90% for optimal locker efficiency, with 1 locker per 10,000 people minimum for network viability.

Delivery Performance Benchmarks: Industry standard 95% on-time delivery rate and 99%+ order picking accuracy for leading e-commerce operations.

Chinese competition. Temu is transitioning to a semi-managed model with 40-50 overseas warehouses planned, potentially bypassing traditional Polish logistics networks entirely. AliExpress launched 10 new European warehouses offering 7-day delivery.

Summary

The relationship between Allegro and InPost has undergone a significant transformation since the beginning of their partnership in 2014. While initially both companies were strongly interdependent, we now observe a process of gradually decreasing this dependency. Currently, my understanding is that Allegro still needs InPost more, but this dependency is slowly weakening. InPost is doing practical & effective work regarding client portfolio diversification and visibility outside Poland.

What will shape this relationship in the coming years includes negotiations of new contracts after 2027, the success of InPost's aforementioned international expansion, the development pace and market share of other platforms like Amazon, OLX, or smaller/alternative entities and platforms. What will consistently play first fiddle are consumer preferences and their evolution. Will the best experience win? And does a lower position in listings already change that experience? Both companies are investing in alternative strategies and testing what awaits them.

Ultimately, while Allegro currently needs InPost more, long-term trends indicate a balancing of this relationship, which may lead to a more symmetric partnership in the future.

That's all that I've for you today. Thank you for taking the time to read this newsletter.

If you enjoyed this text and found value in it, please subscribe to my newsletter. It means a lot to me.

Valuable content deserves to be shared – post the link on LinkedIn, share it on Slack. Tell your friends. This word-of-mouth marketing is the most effective way to reach new readers. I'm just getting started, but I guarantee you'll receive this quality in every future edition.